Is CCSPayment a scam? How to identify real vs. fake debt collectors

CCSPayment is a legitimate payment portal that belongs to Credit Collection Services (CCS). CCS collects debt for various organizations, including credit card companies and healthcare providers. However, there are also numerous reports of scammers impersonating CCSPayment.

Criminals will draft emails and text messages or make cold calls where they impersonate CCSPayment. The goal is to convince a victim to pay them for a nonexistent debt, typically while stealing their personal data in the process.

The problem is that it’s tricky to tell the difference between real and fake debt collectors. To help you avoid falling for a scam, here’s a guide on how to spot fake debt notices and what to do if you’ve already paid a scammer posing as CCSPayment.

What is CCSPayment?

CCSPayment is a name for the online payment portal for Credit Collection Services (CCS), a legitimate debt collection agency created in 1966 and based in Norwood, Massachusetts.

However, there has been some confusion around this, as the company and its platform are now officially called Credit Collection Services, but the name CCSPayment is still used widely online.

Either way, CCS assists creditors in recovering unpaid debts across multiple industries, including medical bills, toll violations, and credit card payments.

Is CCSPayment a legitimate company?

Yes, CCSPayment is a legitimate payment platform operated by CCS, a real debt collection agency. It’s completely safe to visit its website and use its portal to submit payments. It’s also normal for CCSPayment to reach out to its customers, as CCS often contacts people on behalf of companies trying to recover unpaid debts.

However, there is always a risk that someone is impersonating CCSPayment to manipulate you into sending them money, so it’s important to confirm that anyone contacting you is truly affiliated with CCSPayment. If you receive a suspicious debt notice, contact CCS using the official website to verify its legitimacy.

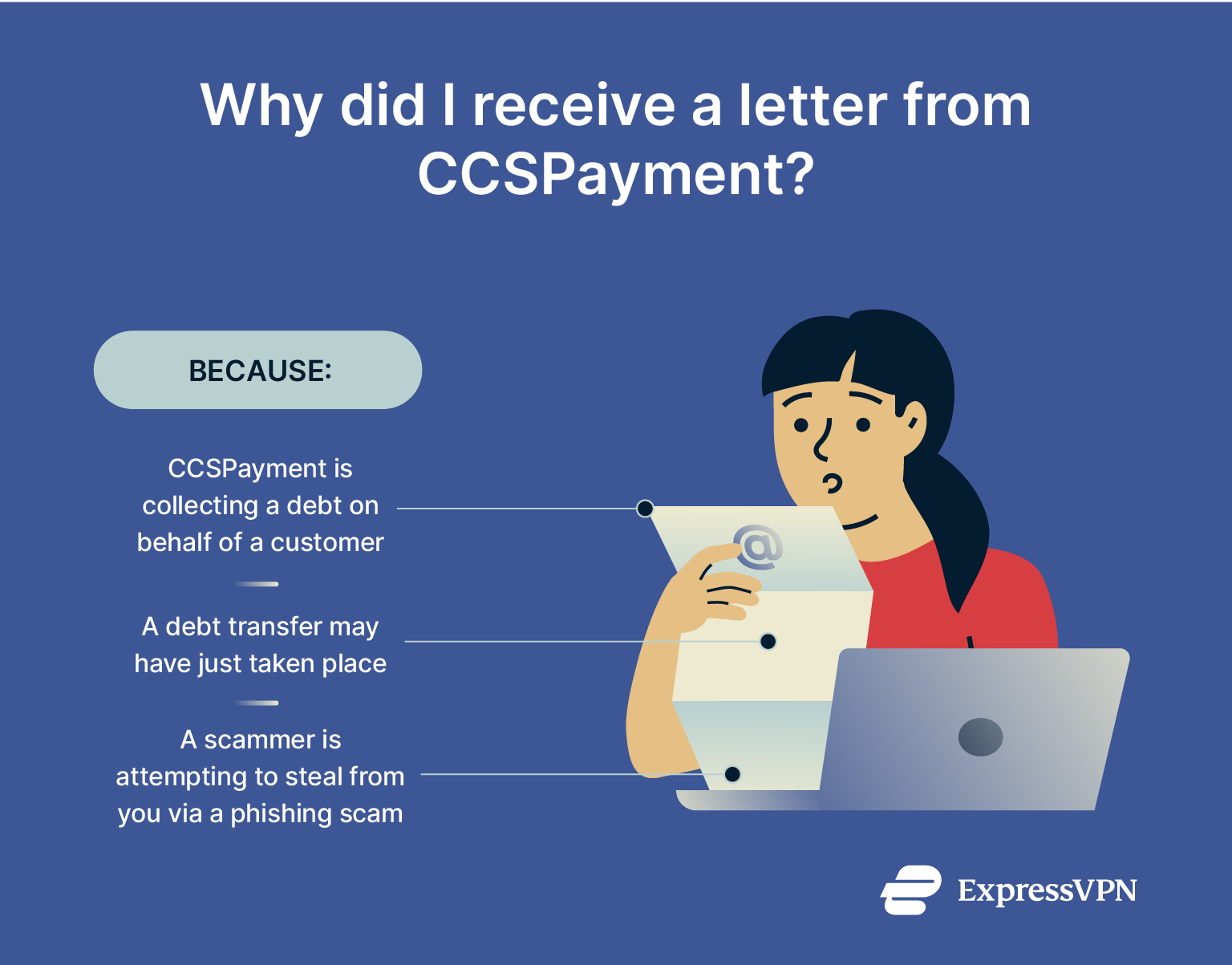

Why did I receive a letter from CCSPayment?

Receiving a letter from CCSPayment usually means that CCS believes you owe a debt on behalf of a creditor. CCS represents customers in a broad range of industries, such as healthcare providers, utility companies, toll agencies, and even credit card issuers. If you owe an outstanding debt to anybody, CCSPayment might be representing them.

Receiving a letter from CCSPayment usually means that CCS believes you owe a debt on behalf of a creditor. CCS represents customers in a broad range of industries, such as healthcare providers, utility companies, toll agencies, and even credit card issuers. If you owe an outstanding debt to anybody, CCSPayment might be representing them.

The letter is typically a formal notification that a debt has been transferred or assigned to CCS for collection and typically includes payment options, a deadline, and instructions for disputing the debt (often by contacting CCS).

In the U.S., the Fair Debt Collection Practices Act (FDCPA) also requires debt collectors to send a written notice within five days of first contact with you, unless that information was already included in the initial communication. This letter must include the amount owed, the name of the creditor, and your right to dispute the debt within 30 days. So, if you received a notice from CCSPayment, know that it's a legally required part of the debt collection process.

However, you might also be contacted by imposters who only claim to represent CCSPayment. Many scammers will impersonate CCS to try and trick victims into believing a false debt so they can steal their money. They often use phishing, a scam where someone impersonates a trusted company or organization to trick victims into sharing sensitive information or sending money.

Could it be a real debt?

Yes, it could be. It’s easy to be surprised by legitimate collection notices due to forgotten accounts, medical bills, unpaid tolls, or an old cash advance. If you've moved, changed insurance, or missed a final bill from a utility company, a debt might have quietly entered collections without your knowledge.

However, you always have the right to request debt validation, which forces the collector to provide proof of the original debt and your responsibility for it. This can help confirm whether the debt is legitimate, correctly attributed to you, and still enforceable under the law.

Can it be a mistake or scam?

Absolutely. It’s completely normal for a debt collection agency to send the wrong person a notice. They might send a warning about collections that have already been paid, have exceeded the statute of limitations, or are no longer legally enforceable. If CCSPayment sent you a warning by mistake, simply contact the company directly to resolve the issue.

It’s also possible that you are the target of a scam. Scammers will often spoof the name of real organizations, like CCSPayment, to send targeted emails, texts, or calls to victims, urging them to pay off their debts. Phishing messages often include a link to a fake website that looks like CCSPayment’s portal but isn’t.

Always verify the legitimacy of any letter you’re sent by visiting the official CCS website and making contact.

Common warning signs of debt collection scams

Knowing the common warning signs of a debt collection scam is the best way to avoid falling victim to one. Here are the most common red flags.

1. You don’t recognize the debt

If you don’t recognize the debt and it doesn’t match anything you owe, be very cautious. Scammers will try to trick you into sending them money to pay off a debt before you’ve had a chance to verify it. If you don’t know what you’re paying off or don’t recognize the company name, contact CCS directly via its official site to check it out.

2. The collector asks for unusual payment methods

One of the worst possible signs is if the collector demands payment through untraceable or difficult-to-reverse methods. This includes wire transfers, gift cards, or cryptocurrency. Real debt collectors should offer traditional payment options (i.e., debit cards). If they refuse normal payment options and push for something unusual, there’s a high chance it’s a scam.

3. They threaten legal action or arrest

Legitimate debt collectors cannot threaten you with jail time simply for owing a debt. If you receive threats of immediate legal action or arrest, it’s certainly a scam (or, at best, it’s a sign of an unprofessional or poorly trained collector).

It’s possible to go to jail for ignoring a judge’s orders surrounding a debt, but you won’t face time for simply having a debt.

4. They threaten your privacy

A real debt collector will never threaten to violate your privacy if you fail to pay them. That’s not legitimate debt collection; it’s blackmail. Sharing debt info with others without permission violates the FDCPA and is illegal. If the collector threatens to share your debt or personal information with family, friends, law enforcement, or the public if you don’t pay, consider it a scam. Under no circumstances should you give them any money.

5. You receive suspicious emails or texts

Be extremely wary of any unsolicited emails or texts where the debtor asks for personal information or payment details. Be particularly suspicious of messages that include a link, as hackers will commonly use links to redirect you to fraudulent websites designed to look like official portals but actually steal your info.

6. They refuse to provide written validation

If a debt collector refuses to provide written verification of the debt within the required 5 days (or the legal timeframe in your country), that’s a huge red flag. Real debt collectors will always offer this proof and respect your right to dispute a debt. If they refuse or seem unwilling to provide the validation, assume it’s a scam, block all communications, and report them.

How to verify if a debt collector is legitimate

Before you mistakenly send money to a scammer, you need to make sure the collector really represents CCS. Here are the steps you should take to make sure the debt is real.

Request a debt validation letter

Under U.S. federal law, debt collectors are required to send a debt validation letter within five days of first contacting you. Failure to provide a debt validation letter is a glaring red flag.

It’s possible that the debt collector simply made an honest mistake by not sending the letter. It also might be so early in the process that they don’t have one yet.

Both cases would be rare when it comes to CCS, however, since CCS is a large and organized company with decades of experience in debt collection.

If you think it really is CCS contacting you but they’re unable to provide a debt validation letter, contact them directly via the official website to inquire further.

Business debts are treated differently. They aren’t typically covered under the same protections that consumers get.

In the U.S., the FDCPA doesn’t provide protection for business debts, so you’re not entitled to a debt validation letter. To validate a business debt, you’ll need to check your local laws, as they can vary dramatically, even on a state-by-state basis.

Verify the phone number and email address

If someone calls, texts, or emails you claiming to represent CCSPayment, you should check their contact information matches that on the official CCS website.

For example, if you’re called by someone informing you about a CCSPayment debt, you can hang up and call back using the official phone number.

If the debt is legitimate, they’ll be able to confirm it using an official number. If they can’t find the debt you’re asking about, you were most likely called by a scammer.

Look for reviews and complaints online

If the name of the creditor you’re supposed to owe money to isn’t familiar to you, check online for reviews about the company in question. Scammers often create fake companies with legit-sounding names.

Search the company name alongside terms like “scam” or “fake” and see what people say. Even the best companies will have a few bad reviews, so try to find a broad consensus. A total lack of online presence can also be a red flag.

You can use tools like the Better Business Bureau (U.S.) or the Financial Conduct Authority (U.K.) to look at aggregated reviews.

Check your credit report

If you have a legitimate debt on your record, it should appear on your credit report. You’re entitled to a free credit report each year from the three major credit bureaus (in the U.S.): Equifax, Experian, and TransUnion. Unless you’ve already requested all three, you can still access at least one report for free.

This will provide a thorough review of what’s affecting your credit behind the scenes. You can see previous loans and debts that you’ve acquired over the years. If the debt on your credit report matches the debt from CCSPayment, there’s a good chance it’s a real debt.

What to do if you suspect a scam

If something feels off, whether it's a phone call, text, or email, trust your gut and stay calm. Here are the steps you should take if you suspect a scam.

Don’t send payment immediately

Even if the notice seems legitimate, take your time to verify that it’s real. Ask the collector to send a formal debt validation letter and don’t pay until you’ve confirmed the debt is real and owed by you. If they won’t send you a formal debt validation letter, they’re almost certainly a scammer.

One of the key signs you’re dealing with a fake debt letter is that the notice is trying to build a sense of urgency. No legitimate collector will pressure you into paying immediately, nor will they immediately resort to threatening legal action if you don’t pay within a short timeframe.

If the collector asks you to use a prepaid solution, cryptocurrency, or a payment processing service that isn’t connected to a bank, you can immediately assume you’re the victim of a phishing scam. Break all contact and report the scam.

Log everything

You should carefully log all communications with the suspected scammer. Save a copy of your entire conversation, letters they sent you, and any suspicious links they sent you.

These crucial details can help law enforcement agencies track down the scammer and prevent them from conning anyone else. It also helps you prove what happened during your official reports.

Reach out to your bank

If you’ve already made a payment to a scammer, it’s a good idea to contact your bank or payment provider and explain the situation. You can ask them to reverse the transaction and give you your money back. Note, however, that success in recovering funds depends on how the payment was made (banks may reverse wire, but not crypto/gift cards).

Report the scam to the FTC or CFPB

If you suspect a scam, report it immediately to the Federal Trade Commission (FTC) at ReportFraud.ftc.gov or the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

These agencies are responsible for tracking and stopping scammers and can sometimes help you recover funds, especially if action is taken quickly. If you make an FTC complaint, they might be able to track down the thieves before they can damage anyone else.

If you’re not in the U.S., report it to your regional government authorities. Most countries have some type of trade agency that oversees consumer trade protections. If you live in the U.K., for example, you can report the scam to Action Fraud (reporting.actionfraud.police.uk).

Report the scam to law enforcement

Next, submit a report to your local law enforcement. It’s important to provide as many details as you can, including the time of the scam, any logs you have saved, financial transactions, and screenshots.

This way, police can open a criminal investigation into the scammer. If the crime is severe enough, or if the perpetrator has multiple victims, multiple agencies will pool resources and work together to find them.

Not only can this lead to the the scammer being identified and charged, but sometimes the police can also recover stolen funds.

Freeze your credit or monitor your accounts

A credit freeze prevents new cards, loans, or accounts from being opened up in your name. If you’ve already shared some of your information with a potential scammer, consider freezing your account through one of the major credit bureaus before they can harm your credit score.

You should combine a credit freeze with credit monitoring tools for more comprehensive protection. These tools will monitor for sudden changes in your credit and help you place a freeze, oftentimes in one or two clicks.

Good credit monitoring tools, like ExpressVPN Identity Defender, alert you when someone takes out a new card or loan in your name. Identity Defender also comes with identity theft insurance.* If a criminal is able to steal your identity as a result of a CCSPayment phishing scam, this insurance works to mitigate the financial damage. Please note Identity Defender is currently only available for users in the US.

How to protect yourself from future scams

Here are a few easy ways to protect yourself from future scams.

Avoid clicking unknown links in emails or texts

Scammers often send phishing emails or texts that appear to be from legitimate companies like CCSPayment. They often create a false sense of urgency or threaten legal action. You can sometimes spot a scam through poor grammar and spelling, but scammers are increasingly using AI to create professional-looking messages.

Always double-check the sender’s address, and never enter personal or financial information unless you're certain the source is authentic.

Look for misspellings in the sender's email address, the lack of a business email account, and any differences between the sender and the official CCSPayment email address. When in doubt, go directly to the company’s official website instead of clicking any links in the message.

Use two-factor authentication for financial accounts

Two-factor authentication (2FA) adds an extra layer of security to your logins by requiring you to use a special code, usually sent to your phone, to access your account.

Enabling 2FA on bank accounts, credit cards, and payment portals helps prevent unauthorized access, even if your credentials have already been compromised.

Additionally, a good password manager helps secure your financial accounts by keeping your passwords, credit card details, and sensitive personal information locked in a secure encrypted vault.

Regularly check your credit reports

Monitoring your credit score can help you spot fraudulent activity early, such as new accounts opened in your name or unexpected debt collections. Most countries have some way to check your credit. For example, in the U.S., you're entitled to a free credit report from each of the three bureaus every year. Consider checking one every four months to keep tabs year-round.

FAQ: Common questions about CCSPayment scams

Can a debt collector text or email me?

For example, in the U.S., the Fair Debt Collection Practices Act (FDCPA) prohibits debt collectors from contacting you before 8 a.m. or after 9 p.m.

Why did CCSPayment contact me?

Can I go to jail for unpaid debt?

Is CCS Collect a real company?

What should I do if I paid a fake debt collector?

How do scammers impersonate debt collectors?

Who does CCS collect debt for?

How do I know if a debt collector’s letter is real?

*The insurance is underwritten and administered by American Bankers Insurance Company of Florida, an Assurant company, under group or blanket policies issued to Array US Inc, or its respective affiliates for the benefit of its Members. Please refer to the actual policies for terms, conditions, and exclusions of coverage. Coverage may not be available in all jurisdictions. Review the Summary of Benefits.

Take the first step to protect yourself online. Try ExpressVPN risk-free.

Get ExpressVPN